Fintech and IT startups in the financial sector are facing a major new regulatory challenge: the EU’s Digital Operational Resilience Act (DORA).

This regulation raises the bar for cybersecurity and operational resilience across banking, payments, crypto, insurance, and more. As a UK-based legal advisory firm (Legal Nodes) serving clients globally, we have seen a surge of interest in DORA compliance from innovative startups who must meet the those new rigorous standards.

In this article, we explain;

- What DORA is and why it was introduced;

- Who needs to comply;

- The risks of non-compliance, and the key legal, operational, and technological aspects of DORA.

We also provide practical insights for small companies implementing DORA and a recommended roadmap to achieve compliance – including how our firm can support you from initial gap analysis to full documentation.

What Is DORA and Why Was It Introduced

DORA (Digital Operational Resilience Act) is a landmark European Union regulation designed to strengthen the financial sector’s ability to withstand and recover from IT disruptions and cyberattacks[1]. Officially adopted as Regulation (EU) 2022/2554 in late 2022, DORA took effect on January 17, 2025 after a two-year implementation period.

DORA was introduced in response to growing digital risks in finance.

In recent years, banks, payment firms, insurers, and fintech startups have become highly reliant on cloud services, software platforms, and other technologies. This has led to a corresponding rise in cyber threats, IT outages, and incidents that could threaten not just individual companies but the stability of the entire financial system. Prior to DORA, EU countries had a patchwork of cybersecurity rules, leading to inconsistent resilience levels. High-profile incidents and the fragmented regulatory landscape made it clear that a unified approach was needed. DORA’s goal is to harmonize and upgrade operational resilience standards across the EU financial sector, creating uniform requirements for managing ICT (information and communication technology) risks. By establishing a single, comprehensive framework, DORA aims to prevent and mitigate cyber threats through better preparation, coordinated response, and stronger defenses in every financial entity.

In essence, DORA mandates that financial companies proactively manage their digital risks and remain operationally resilient even under severe IT stress. This includes having robust governance over ICT risks, incident response plans, backup systems, and cybersecurity controls. DORA fills a critical gap not addressed by traditional financial regulations – recognizing that a cyber incident can’t be averted by capital buffers alone, but by proper ICT risk management.

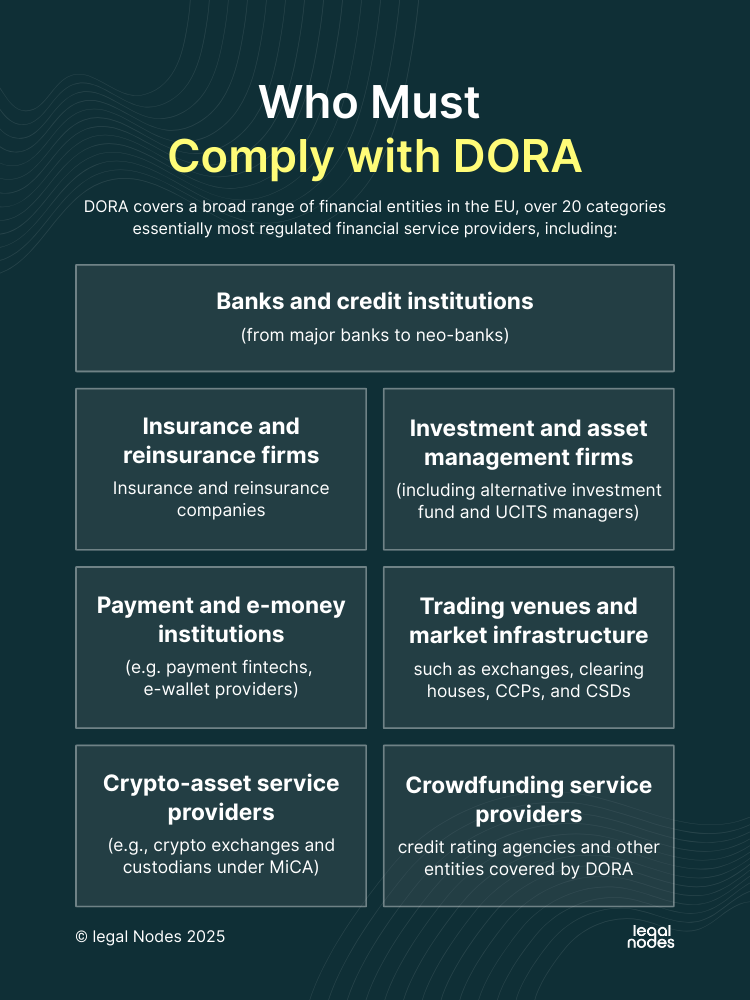

Who Must Comply with DORA

DORA casts a wide net over the financial sector. It applies to 20+ categories of “financial entities” in the EU, essentially covering most regulated financial services firms. This includes:

- Banks and credit institutions (from major banks to neo-banks),

- Insurance and reinsurance companies (and certain insurance intermediaries),

- Investment firms and asset managers (including alternative investment fund managers and UCITS managers),

- Payment institutions and e-money institutions (e.g. payment fintechs, e-wallet providers),

- Trading venues and market infrastructures such as stock exchanges, clearing houses, central counterparties, and central securities depositories,

- Crypto-asset service providers (e.g. crypto exchanges and custodians, as brought into scope by EU’s MiCA regulation),

- Crowdfunding service providers, credit rating agencies, and other financial sector entities enumerated in DORA’s scope.

In short, if your startup is operating in the EU financial sector with any form of regulatory license, it is likely subject to DORA. Even many fintech startups (e.g. payments or lending platforms, digital insurers, crypto exchanges) fall under these categories and must meet DORA’s requirements just like traditional banks. Notably, DORA’s scope extends to pension funds and alternative investment funds as well, which underscores how comprehensive the coverage is compared to some domestic regimes. (For perspective, the UK’s own operational resilience rules cover banks and insurers but do not automatically include asset managers or crypto firms, whereas DORA does.)

What about IT companies and third-party tech providers?

DORA recognizes that financial institutions rely on a complex web of third-party ICT services – from cloud infrastructure and software platforms to data analytics providers.

Critical ICT service providers that serve financial entities can be directly brought under DORA’s oversight. In particular, if a tech firm is designated as a “critical ICT third-party provider” (CTPP) due to the essential services it offers to the financial sector, it will be subject to strict regulatory oversight by European Supervisory Authorities. Even if not formally designated as critical, ICT providers are impacted indirectly – financial institutions must ensure all their vendors meet DORA-aligned standards through contractual terms and ongoing monitoring. Importantly, location is no shield:

DORA applies to ICT providers even outside the EU if they serve EU financial entities. For example, a UK or US cloud company supporting an EU bank may find that bank pressuring it to adapt to DORA requirements, and if the provider is deemed critical, EU regulators could oversee parts of its operations.

In summary, companies that must be DORA-compliant include almost every type of regulated financial institution in the EU, as well as the tech firms that keep financial businesses running. Fintech and IT startups should carefully determine if they fall in scope (DORA’s Article 2 lists all entity types). In doubt, assume you are covered unless you clearly meet an exemption (few narrow exemptions exist – e.g. very small insurance intermediaries, certain AIF managers, or specific microenterprises as discussed later).

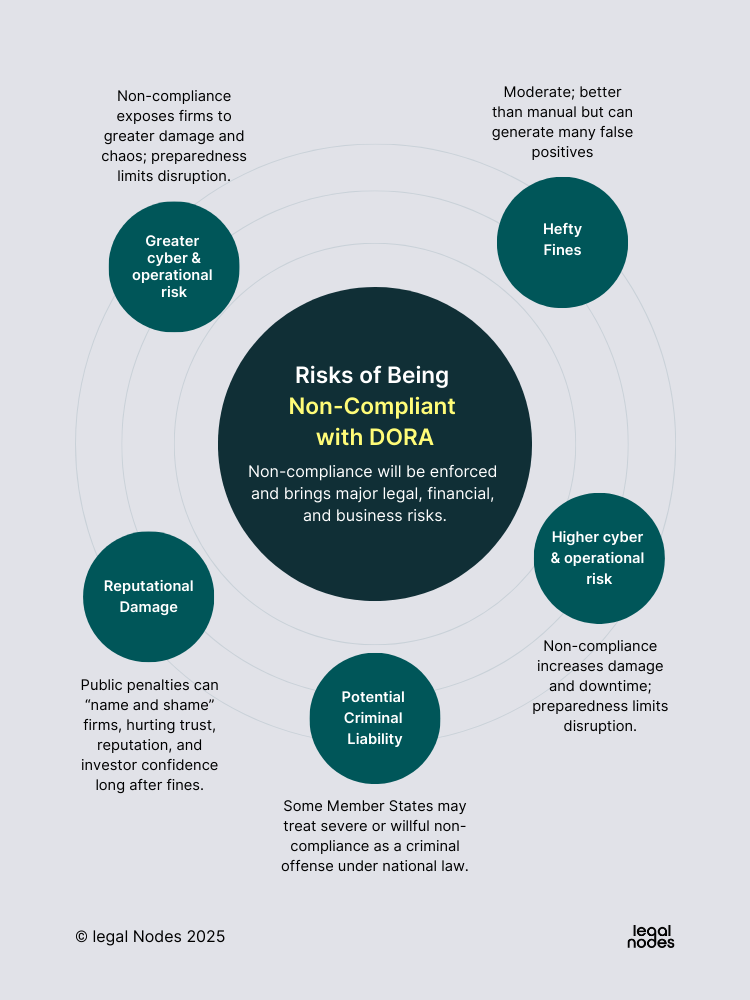

Risks of Being Non-Compliant with DORA

Failure to comply with DORA is not an option – the risks of non-compliance are severe from legal, financial, and business perspectives. Regulators across EU Member States will enforce DORA vigorously once it applies, and companies falling short can face a range of penalties and consequences:

- Hefty Fines: Financial regulators are empowered to levy substantial fines for non-compliance. Under DORA’s framework, financial entities may be fined up to 2% of their total worldwide annual turnover for breaches of the requirements. For large institutions, this could amount to millions of euros. Critical third-party providers face fines as well – up to €5,000,000. There is also a mechanism for daily penalties up to 1% of average daily turnover for each day of continuing non-compliance (for up to six months). In practical terms, a mid-sized fintech or bank that remains non-compliant for months could accrue multi-million euro penalties, far outweighing the costs of compliance.

- Administrative Sanctions & Business Restrictions: Beyond fines, regulators can impose corrective measures and sanctions. This can include issuing binding orders to remedy deficiencies and, in extreme cases, suspending or limiting a firm’s operations. DORA explicitly allows authorities to restrict a company’s business activities or even suspend authorizations/licenses if persistent or severe non-compliance jeopardizes the firm’s stability. Regulators may also suspend or prohibit a financial entity from engaging a particular ICT provider if that provider poses unacceptable risk and fails to address deficiencies. In other words, a bank could be forced to drop a non-compliant cloud vendor, or a fintech could be ordered to cease offering certain services until it fixes its controls. For startups, such enforcement actions could be existential threats.

- Reputational Damage: Regulatory penalties under DORA will not remain private. Authorities have the power (and incentive) to publicize enforcement actions – essentially “name and shame” organizations that violate DORA. For example, if a data breach occurs and a firm is found non-compliant, a public notice could be issued detailing the firm’s failures. This kind of publicity can severely erode customer trust and damage a brand’s reputation. Being labeled as falling short on operational resilience is likely to scare off investors, counterparties, and customers, causing long-term business harm beyond the immediate fine.

- Heightened Cyber and Operational Risks: Aside from regulatory reprisals, being non-compliant with DORA essentially means a firm lacks adequate defenses and plans for cyber incidents. That itself is a huge risk. A company that delays compliance may find itself ill-prepared for a serious outage or attack, leading to longer downtime, larger financial losses, and panicked scrambling when an incident occurs. In contrast, compliance efforts (like robust incident response and business continuity plans) greatly reduce the impact of disruptions. In short, non-compliance leaves an organization exposed – if a major ICT incident hits, the firm will suffer more damage and have fewer defenses, a risk no responsible fintech startup or financial institution should accept.

- Potential Criminal Liability: While DORA itself does not stipulate criminal penalties at the EU level, it requires Member States to set their own penalty regimes. Some countries may choose to treat extreme negligence or willful non-compliance as a criminal offense in national law.

In summary, the cost of non-compliance far exceeds the cost of compliance. DORA enforcement can hit violators with crippling fines, legal sanctions, public reputational blows, and even operational shutdowns. For fintech and IT startups aiming to build customer confidence and partnerships in the financial industry, being non-compliant would be disastrous. Regulators have signaled that they will not hesitate to use DORA’s enforcement tools to ensure the financial sector is safe from digital disruption. The clear takeaway is that proactive compliance is the only viable path – and indeed, a firm that meets DORA standards will not only avoid penalties but also benefit from improved security and resilience.

Legal, Operational, and Technological Aspects of DORA Compliance

Achieving DORA compliance is a multidisciplinary effort. It’s not just a legal box-ticking exercise or an IT upgrade; it spans governance (legal), daily processes (operational), and infrastructure/security (technological) changes. Let’s break down each aspect:

- Legal & Governance: DORA introduces formal legal obligations and governance requirements that organizations must embed at the top levels. Every in-scope company must establish a strong internal ICT risk management framework overseen by the board and senior management. The management body is explicitly accountable for digital operational resilience – they must approve and periodically review strategies and policies, and ensure compliance is integrated into the overall risk management of the firm. In practice, this means new or updated policies, protocols, and documentation: e.g. an ICT risk management policy, incident response plan, business continuity plan, third-party risk management policy, etc., all aligned with DORA’s detailed requirements. These documents need regular review and approval at board level. Contractual arrangements also fall under the legal aspect – firms must review and amend contracts with technology providers to insert mandatory DORA provisions. For instance, outsourcing agreements should include clauses on security measures, audit rights, incident reporting duties, and termination rights as required by DORA. Legal teams will need to ensure contracts, vendor due diligence processes, and even things like insurance coverage reflect the new resilience standards. Overall, compliance must be anchored in governance: clear roles and responsibilities, management oversight, and a culture of risk awareness and accountability at all levels.

- Operational Processes: DORA compliance significantly impacts day-to-day operational practices and risk management processes within an organization. Firms must implement a comprehensive ICT risk management program and have a robust incident management process: the ability to detect and swiftly classify, log, escalate, and report ICT-related incidents in line with DORA’s criteria. Timely reporting to regulators is mandated for major incidents (with tight timelines akin to those in cybersecurity laws like NIS2 – initial notification within hours). Periodic resilience testing is another operational piece: DORA requires regular testing of systems and controls, ranging from vulnerability scans and penetration tests to scenario-based drills. Larger institutions may even need advanced threat-led penetration testing on critical systems. Firms must maintain an up-to-date register of all ICT third-party service providers and the critical functions they support, monitor their performance, and have exit strategies in case a vendor fails. This involves operational coordination between procurement, IT, and risk teams to assess vendor resilience. In essence, DORA forces organizations to embed resilience into every routine – from how changes to IT systems are managed, to how staff are trained to handle incidents. Compliance will require refining standard operating procedures and conducting training and drills so that everyone knows their role when an incident strikes.

- Technological Measures: There is a heavy IT and security component to DORA compliance. Financial entities must ensure that their hardware, software, networks, and data are protected and resilient in line with state-of-the-art practices. This means implementing technical controls such as encryption, access management, and regular patching of vulnerabilities. DORA also expects firms to maintain reliable and geographically distributed backup systems for critical data and functions. Monitoring systems for anomalous activities is another key technology aspect. Firms might deploy intrusion detection systems, SIEM (Security Information and Event Management) tools, or other monitoring solutions to continuously watch for signs of cyber intrusions or system stress. Incident response tooling (like centralized logging, forensics tools) should be in place to investigate and respond when alarms trigger. On the resilience side, companies should invest in architecture improvements such as eliminating single points of failure (through load balancing, clustering, or cloud failover capabilities), and ensuring capacity can handle peak loads or DDoS attacks. Regular testing of defenses technologically may involve automated vulnerability scanning, penetration testing by external experts, and scenario simulations (e.g., simulating a ransomware attack to see if systems and staff respond appropriately). Additionally, technological standards for third parties need oversight – e.g. ensuring a cloud provider has certifications like ISO 27001 or meets DORA’s “appropriate security standards” clause in contracts. The bottom line is that IT infrastructure and cybersecurity capabilities must be robust and up-to-date. For tech-focused startups, aligning with DORA might simply mean formalizing and documenting practices they already consider good hygiene. But for any firm, continuous technological vigilance and improvement are now a regulatory imperative, not just an IT concern.

Achieving DORA compliance means working across departments: legal/compliance, IT, cybersecurity, operations, risk management, and senior leadership must collaborate. It’s a challenging effort, but ultimately it will strengthen the organization’s resilience and trustworthiness.

Practical Insights for Implementing DORA in Small Companies

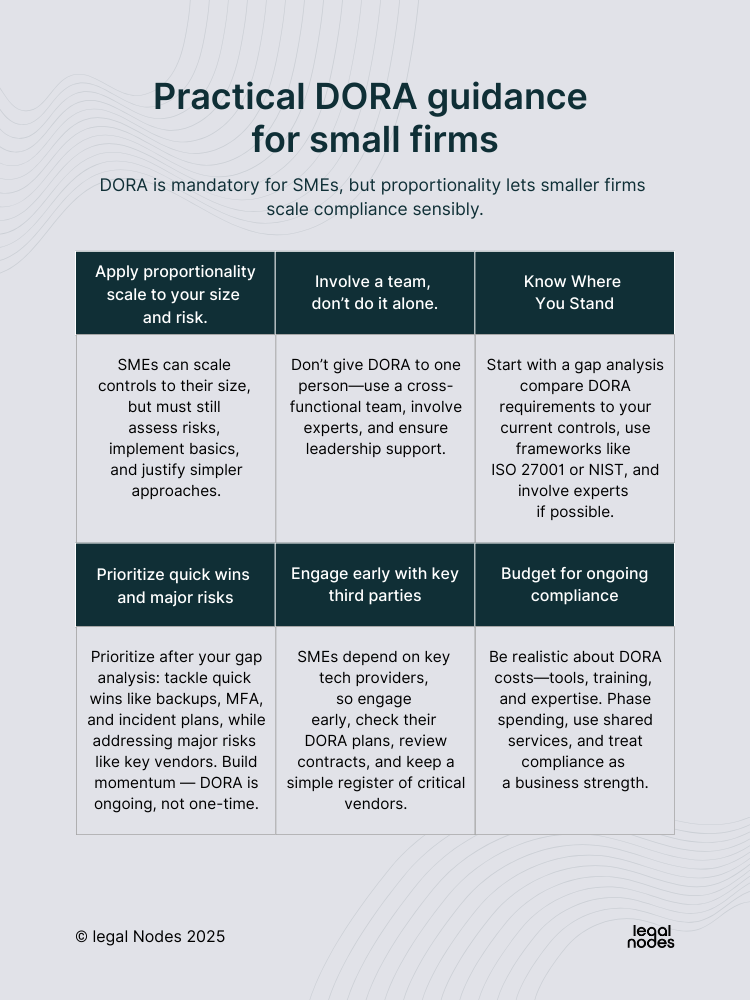

Implementing DORA can be daunting for small and medium-sized enterprises (SMEs), such as fintech startups or boutique financial firms. Unlike big banks, smaller companies have limited resources and often less experience with extensive regulatory frameworks. Indeed, many SMEs are finding it challenging to “keep up” with DORA’s vast requirements, whereas larger legacy institutions have been preparing for years. However, small companies must comply – DORA does not exempt firms just because they are small. The good news is that DORA builds in principles of proportionality and flexibility that can help scale the effort appropriately for an SME. Here are some practical insights and tips for smaller organizations approaching DORA compliance:

- Leverage Proportionality – Scale Requirements to Your Size and Risk: DORA explicitly acknowledges that one size does not fit all. Article 4 of DORA establishes a proportionality principle, stating that regulators will consider a firm’s size, risk profile, and the nature/complexity of its business when assessing compliance. In practice, this means smaller institutions and startups are not expected to have the same depth of resources and elaborate systems as a global bank. For example, a two-person fintech startup won’t need a 100-page risk report or an in-house red-team for penetration testing. Some requirements may even be simplified for microenterprises (typically defined as firms with <10 employees and <€2M turnover) – DORA grants certain lighter obligations for these very small entities. However, proportionality is not an excuse to do nothing; even an SME must demonstrate it has assessed its risks and taken appropriate measures, just on a smaller scale. Tip: Focus on the most critical risks and core requirements first. Implement the fundamentals (like an incident response plan, backups, basic security controls) thoroughly, and document why more complex measures might be disproportionate. Regulators will likely accept scaled-down approaches as long as they are reasonable for your profile.

- Don’t Go It Alone – Involve a Cross-Functional Team and External Help: One common mistake for startups is leaving DORA compliance to a single IT manager or an overstretched COO. In reality, DORA touches many parts of the business, so you need a broad team to tackle it. Assemble a working group that includes IT/security personnel, operations staff, risk/compliance officers, and someone from leadership. If you don’t have in-house specialists, consider engaging external experts or advisors to fill those gaps. External consultants can provide templates, technical know-how, and an outside perspective to jumpstart the process. Importantly, ensure top management is on board – leadership support is critical to allocate resources and drive a culture of compliance. By spreading responsibilities across a team, SMEs can avoid overburdening one person and ensure that all aspects (from legal documentation to IT fixes) get proper attention. Tip: Hold cross-department meetings or workshops on DORA readiness. This breaks silos and builds a shared understanding of resilience across the company.

- Know Where You Stand: For any company, and especially SMEs new to such regulation, the first actionable step is to conduct a thorough gap analysis. This means mapping out all of DORA’s requirements and comparing them against your current policies, procedures, and controls. The gap analysis will highlight where you are already compliant (perhaps by virtue of existing cybersecurity practices) and where the gaps are. It can be time-consuming to parse the entire regulation, but it’s an essential foundation to plan your compliance project. You can also leverage frameworks like ISO 27001 or NIST CSF you might already follow; map those controls to DORA’s areas. If budget permits, bring in a consultant or legal expert like Legal Nodes team to perform a professional gap assessment.

- Prioritize “Low-Hanging Fruit” and Biggest Risks: Not all DORA tasks are equal. Some measures will be relatively easy to implement and yield high value (the “low-hanging fruit”), while others might be heavy lifts. After your gap analysis, prioritize the compliance actions. For a small firm, quick wins might include: writing an incident response plan (if you lack one), setting up an automated cloud backup, enabling multi-factor authentication for all logins, or instituting basic staff cybersecurity training. These are relatively straightforward and greatly improve resilience. In parallel, identify your most critical vulnerabilities or risk areas – for example, if your whole business relies on one third-party cloud service, that dependency is critical. Focus on getting contingency plans for it, and engage with that vendor about their resilience. By tackling the important and achievable steps first, you build momentum and reduce key risks sooner. Tip: It’s fine to take an iterative approach. DORA compliance is not a single project you finish and forget – it’s about continuous improvement. Do the essentials now and plan to refine and expand measures over time.

- Engage Early with Key Third-Party Providers: Small fintechs often rely heavily on a handful of tech providers (cloud hosting, payment processors, core banking software, etc.). Your operational resilience is only as strong as theirs. DORA will indirectly pressure these providers through contractual obligations and oversight. A practical step is to reach out to your critical vendors sooner rather than later. Ask them how they are preparing for DORA (the big ones will have a strategy). Many large providers are creating DORA compliance addendums or templates for their contracts. If you receive one, review it carefully (or have counsel review) to ensure all required clauses are included. If you have any negotiating power (perhaps if you’re a significant client or still in contract negotiation), insist on DORA-aligned terms like uptime guarantees, audit rights, and subcontractor risk controls. The earlier you renegotiate or update agreements, the better. Tip: Document all your third-party services in a simple register (if you haven’t already). For each, record whether it supports any critical function of yours. This will help satisfy DORA’s requirement for a register of ICT providers and also highlight which vendors to prioritize for outreach and contingency planning.

- Budget and Plan for Ongoing Compliance Costs: Small companies need to be realistic about the investment needed for DORA compliance. There could be costs for new security tools, consultants or auditors, staff training, and possibly hiring additional IT/security personnel. While budgets are tight, consider the cost of non-compliance (fines, incidents) as the alternative. It may be useful to phase expenditures – e.g., invest in the most essential technology upgrades in year one and plan for advanced testing (like an external penetration test) in year two. Also explore shared solutions: if hiring a full-time cybersecurity expert isn’t feasible, maybe use a virtual CISO service or managed security service to cover the need. Tip: Treat DORA compliance as an opportunity to build a stronger company. The processes you put in place can improve efficiency (for example, incident reporting mechanisms can double as customer support processes during outages). Demonstrating robust operational resilience can also be a selling point to investors or clients – it shows maturity and reliability.

In conclusion

DORA represents a significant new benchmark for operational resilience in the financial industry. Fintech and IT startups should view compliance not just as a legal obligation but as an investment in their own robustness and credibility. By knowing what DORA requires, who it impacts, and how to comply across legal, operational, and tech dimensions, you can turn this challenge into an opportunity to strengthen your company. And remember – you don’t have to do it alone. With the right roadmap and the right advisors by your side, DORA compliance is entirely within reach, positioning your startup to thrive in a safer, more resilient digital financial ecosystem.