As a business owner, one of the most significant milestones is structuring your own compensation.

When your company operates in a different country from where you live, this decision becomes a complex puzzle of international tax law.

Getting this wrong can lead to high tax bills, penalties, and stressful disputes with tax authorities. Getting it right ensures you are rewarded for your contribution efficiently and sustainably.

This guide breaks down the essential tax considerations for founders receiving income from their foreign companies.

Determining the Right Structure for Your Payout

The first step is deciding how to pay yourself.

While founders often start with one method, the most efficient strategy usually involves a mix. The most common methods are salary, director's fees, consulting fees, and dividends, each with vastly different implications.

Salary

This is compensation you receive for the operational work you perform for the company (e.g., as CEO, developer, or manager).

Implications:

- For the Company: A salary is typically a tax-deductible business expense in the company's jurisdiction, reducing its taxable profits.

- For You (the Founder): This is where the risk lies. Salary is often subject to two layers of tax and contributions:

a. Source Country: The company's jurisdiction may levy payroll taxes and social security contributions.

b. Residence Country: You must then report this as employment income in your home country, where it will be subject to personal income tax and potentially another layer of social security. This can be the most tax-inefficient method if not structured carefully.

Director's Fees

This is compensation you receive for your governance role as a member of the Board of Directors. It is for strategic oversight, not day-to-day management.

Implications: The distinction from salary is crucial. Director's fees often have different tax treaty rules, which may change where they are taxed (e.g., often taxed in the company's jurisdiction).

Consulting Fees

This involves your foreign company paying you (or your local sole proprietorship) for specific, project-based consulting services under a service agreement.

Implications:

- Flexibility: This is a very common method for early-stage startups, as it's flexible and can be a deductible expense for the company.

- High Risk: Tax authorities heavily scrutinize these arrangements. If it looks like a "disguised salary" (e.g., you're the only "consultant" and you work full-time), they can re-characterize the income as employment, leading to back-taxes and penalties.

- Defense: This structure is most defensible if you genuinely run a consulting business and provide similar services to other, unrelated clients.

Dividends

This is a distribution of the company's profits to you as a shareholder (an owner).

Implications:

- For the Company: Dividends are not a tax-deductible expense. They can only be distributed if the company has sufficient after-tax profits (or retained earnings) available for distribution.

- For You (the Founder): Like salary, dividends are subject to two layers of tax:

a. Withholding Tax (WHT) in the Source Country: The company's jurisdiction will often levy a WHT on the dividend payment before it leaves the company's bank account.

b.Income Tax in Your Residence Country: You must then report this foreign dividend income on your personal tax return in your home country and pay tax on it.

- The Benefit: Despite the two layers, the total effective tax rate on dividends is often lower (preferential) than on salary income, and dividends are typically not subject to social security contributions.

What Payout Structure Should You Choose?

The Verdict

There is no single "best" answer. The most efficient choice depends entirely on your personal situation and the specific tax laws in two key places:

- Your Company's Jurisdiction: (What is the corporate tax rate? What is the WHT on dividends?)

- Your Personal Tax Residency: (What are the tax rates for salary vs. Dividends vs. consulting fee vs. director’s fee? How does the Foreign Tax Credit work? What are the social security rules?)

A strategy that is tax-efficient in one country could be a costly mistake in another. This highlights the importance of strategic planning, as these tax consequences can often be optimized by correctly choosing the jurisdiction for your company registration or even planning a personal relocation.

The Core Challenge: Tax Residency and Double Taxation

Understanding how you are taxed is impossible without first knowing where you are taxed. This is the foundation of all international tax planning.

What is Tax Residency and Why Does it Matter?

Your tax residency determines which country has the primary right to tax your worldwide income. It is not the same as your citizenship. It is a legal status determined by objective facts like did you spend more than 183 days in a single country during its tax year, where you have a permanent home, where your family lives, and where your "center of vital interests" is.

Your country of tax residence (e.g., Poland) generally claims the right to tax you on all your income, from all sources, worldwide.

The Double Taxation Risk This immediately creates a conflict.

- Your company's country (Country A) wants to tax the income generated there (via payroll tax, WHT, etc.).

- Your residence country (Country B) wants to tax you on that same income because you live there.

This is double taxation , and without a solution, you could pay a total tax of 40-60% on your income.

How to Mitigate It: Double Tax Treaties (DTTs) To prevent this, countries sign Double Tax Treaties (DTTs). These are bilateral agreements that set the rules for "who taxes what". They provide two primary solutions:

- Reduced Withholding Tax: The treaty may lower the tax rate the source country (Country A) can charge. For example, a country's standard dividend WHT might be 30%, but a treaty could reduce it to 10% or 5%.

- Foreign Tax Credit (FTC): This is the most common solution. Your home country (Country B) will still tax your foreign income, but it will allow you to take a credit for the tax you already paid to Country A.

To claim these benefits, you cannot just tick a box. You must proactively prove your tax residency to the foreign company's country, typically by providing a formal Tax Residency Certificate from your home tax authority.

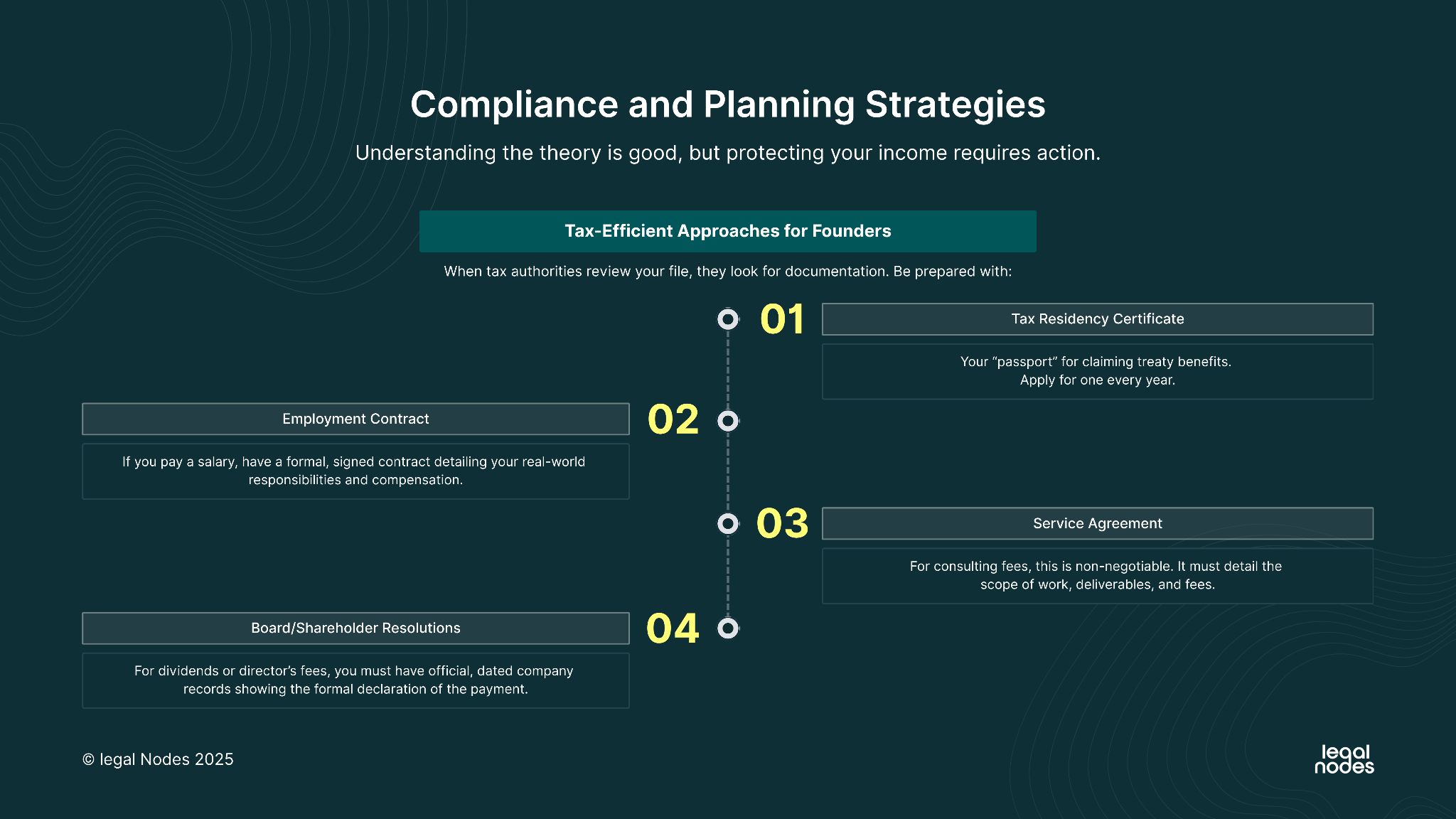

Compliance and Planning Strategies

Understanding the theory is good, but protecting your income requires action.

- Documentation is Your Shield : When tax authorities review your file, they look for documentation.

Be prepared with:

- Tax Residency Certificate: Your "passport" for claiming treaty benefits. Apply for one every year.

- Employment Contract: If you pay a salary, have a formal, signed contract detailing your real-world responsibilities and compensation.

- Service Agreement: For consulting fees, this is non-negotiable. It must detail the scope of work, deliverables, and fees.

- Board/Shareholder Resolutions: For dividends or director's fees, you must have official, dated company records showing the formal declaration of the payment.

- Tax-Efficient Approaches for Founders

- The Optimal Mix: The most efficient strategy is often not "all or nothing." It may be a strategic combination of a (reasonable) base salary to cover living expenses, topped up with dividend distributions in profitable years.

- Strategic Timing: You control when your company distributes a dividend. You can time these distributions for maximum efficiency—for example, avoiding a large dividend in a year when you also have other high-income events.

- Holding Company Structures: For more complex businesses, founders may establish a holding company to own the shares of their operating companies. This can centralize profit, defer tax, and make future sales of the business more efficient, though it adds cost and compliance.

Final Thoughts

Paying yourself from your foreign business is a critical step in your entrepreneurial journey. By understanding the core differences between payment methods, confirming your personal tax residency, and proactively using tax treaties to mitigate double taxation, you can build a compliant and efficient remuneration strategy.

The rules are complex and jurisdiction-specific. This highlights the importance of strategic planning, as these tax consequences can often be optimized by correctly choosing the jurisdiction for your company registration or even planning a personal relocation. Investing in professional tax advice tailored to your specific situation is the best way to protect your hard-earned income.